Partner Organizations

Development Partners

The Platform for Collaboration on Tax is also supported by the governments of

France

Japan

The Netherlands

Norway

Switzerland

United Kingdom

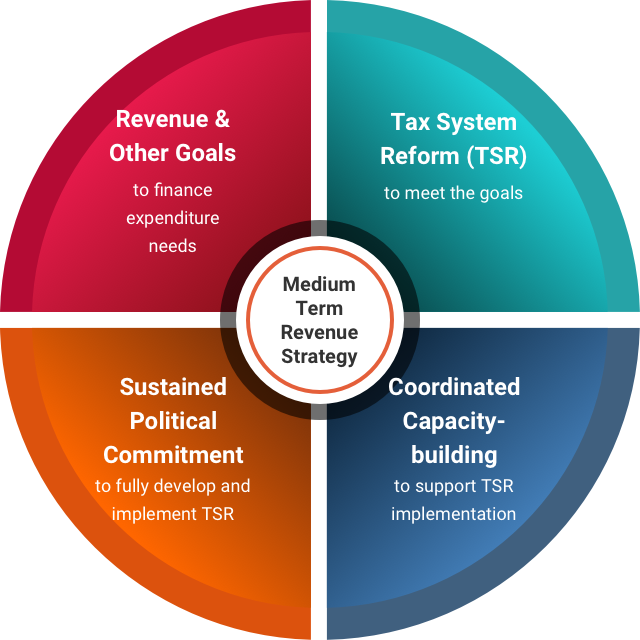

The Medium-Term Revenue Strategy is a comprehensive approach for undertaking effective tax systems reform for boosting tax revenues and improving the tax system over the medium term through a country-led and whole-of-government approach. The MTRS was introduced in the 2016 PCT report on Enhancing the Effectiveness of External Support in Building Tax Capacity in Developing Countries. More information about the MTRS can be found below.

A medium-term and comprehensive approach to reform the tax system’s components is beneficial because:

The MTRS provides a setting to achieve all these critical goals. An MTRS does not mean that benefits come only in the medium-term; it also provides the setting for short-term measures that are of high quality and consistent with the vision of fundamental improvement.

Presently, 25 countries are engaged with Partners in discussing, formulating or implementing an MTRS. See the latest list of countries discussing MTRS.

The MTRS has four interdependent components.

Some 25 countries are currently involved in discussing, formulating, and implementing MTRSs. These countries receive extensive support for their MTRSs from PCT Partners, in particular, the IMF and World Bank who can leverage their typically large presence at the country level. Many countries are already fully engaged in tax administration, law and/or policy reforms domestically that provide a sound basis for adopting a holistic approach–particularly one integrated with and based upon an analysis of development spending needs. In some cases, these ongoing reforms are taking place through intensive engagements financed, for example, under the IMF’s Revenue Mobilization Thematic Fund (RMTF) or World Bank’s Global Tax Program (GTP). In other cases, for instance, the UN supports MTRSs through its linkages with the Sustainable Development Goals while OECD provides support in some countries by training on international tax, exchange of information and the Tax Inspectors Without Borders (TIWB) program.